Rent vs Buy — What’s right for you?

Most people in my age group are either getting married, moving out for the first time — or wondering how the heck they are going to do either one of those two. I thought it would be useful to share my own experience and analysis on why I decided to rent my first home. Thank me later 🙂

My current accommodation

Currently living in Toronto, my analysis below will be based on the downtown Toronto real estate market. You could expect the numbers to vary quite a bit on a city by city basis, but the premise will be the same.

My wife and I currently live in a 1 + den at 10 York St. It is an amazing Tridel built building, with quality features from top to bottom. Aside from minor mishaps on the elevator, we have not noticed much that could really be improved in this building (which is quite impressive given some of the real estate that is being built in Toronto today).

We pay a total rent of $2,350 per month, not including utilities or parking. To maintain an apples to apples comparison, let’s focus our analysis on this standalone amount.

Current rent: $2,350 for a 1+D in the heart of downtown Toronto.

Do we buy or do we rent?

I played around with this thought in my mind quite a few times, do we rent or do we buy.

When I started to look into the numbers, I could not tell if my analysis was wrong or if purchasing a home in downtown Toronto was going to be a terrible investment — contradictory to what almost every single person in the city of Toronto will tell you.

Based on my math I would have saved around $1.5K a year if I put about $35K as a down payment. The return on investment (ROI)? About 4.2% a year, which is really just inflation in my eyes.

To put it simply and save you quite a bit of reading, if you do not think you can get better than 4.2% return on your money then buying a condo would make sense. However, if you can, your money is best deposited elsewhere. If you don’t know how to get more than 4.2% — ask me how; my lowest rate of return on my current investments is 12%, so I am happy to help.

There is going to be a fair number of people that will wonder how I arrived at these numbers, which is completely fair. So lets break it down — and please do challenge me, lets talk!

My wife and I currently live in a 1 + den at 10 York St. It is an amazing Tridel built building, with quality features from top to bottom. Aside from minor mishaps on the elevator, we have not noticed much that could really be improved in this building (which is quite impressive given some of the real estate that is being built in Toronto today).

We pay a total rent of $2,350 per month, not including utilities or parking. To maintain an apples to apples comparison, let’s focus our analysis on this standalone amount.

The Potential “Purchase”

Based on the sold data as at December 2019; I found the average purchase price for a 1+den in this condo to be about $700K. This would be a similar size unit, no parking, no locker and on the 27th floor which is close enough to my own. Lets be a bit aggressive and say I could find one for $680K because who likes paying market price. Add in some closing costs, in Toronto ~ 20K; ending purchase price: $700K.

I’m going to assume I would have put 5% ($35K) down, because the thought of having to put $140K down to buy a home for myself that I am not going to get any cash flow from, is quite painful. Scroll down to the bottom if you would have put 20% down — I don’t really think it changes a whole lot but I look at ROI which is based on how much of my capital is injected.

The rest ($665K plus the mortgage insurance of $26.6K, totaling $691.6K) would be financed by a mortgage from one of the many lenders out there, likely for a rate in today’s economy of about 2.7%. That $691K mortgage would amount to a $3,170 per month payment. (This is based on a 25 year amortization period because I’m going less than 20% down, different online calculators will give you slightly different numbers +/- $50).

So here is some quick basic math, this is the last bit of technical math.

Payment: $3,170 per month = $38K per year; made up of principal ($19.6K) and interest ($18.4K). Here is useful tool for anyone that wants to do the calculation themselves.

Expense 1: Mortgage Interest: $18.4K

One of the benefits of living in a condo, you have no roof, no need to shovel the snow or cut the grass, you have this awesome pool and a gym you rarely use. But you pay for all this in the form of a maintenance expense — which is fair, because you pay for what you enjoy. If you rent — you aren’t directly paying for this, but if you own, you are.

In my condo — based on the MLS, it looks like common area maintenance expense would be about $350.

If you don’t live in a condo, view this as the amount of money you would have to spend on your own roofing, grass cutting, cap ex etc for your house.

Expense 2: Common Area Maintenance: $350 per month = $4.2K

AH and we live in the beautiful city of Toronto. So, of course — you pay to live. Based on MLS again your property tax would be about $3020.

Expense 3: Property Taxes: $3K per year.

The above does not account for the wear and tear on the property, the cost of replacing appliances etc. For simplicity, let us use a blended rate of 3% to cover for repairs and maintenance (painting, landscaping etc) and capital expenditure (roof, appliances, flooring etc). Some people would argue 3% is quite low, but I am using it since this is an owner occupied home.

Expense 4: Total R&M and Capex budget would be 3% of rental revenue = $846 per year.

Total Expenses if you buy a condo in the heart of Downtown: ~$26K

Monthly Expense from Purchasing: $2,228.

Currently my rent expense is $2350 per month.

This means if I were to purchase my home, I would save $122 per month. Annualized this is $1.5K. The logic of most Torontonians is put $35K down to save this $1.5K per year; which is about 4.2% ROI.

It is up to you to determine if a 4.2% ROI(or what ever number you generate for your city) is worth the investment for you — it is not enough for me 🙂

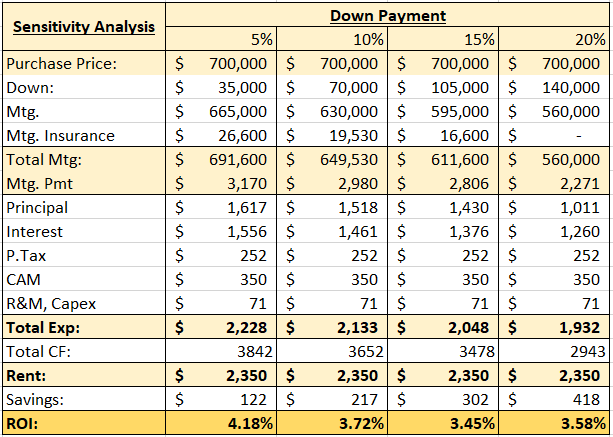

“What if i put 20% down”

For anyone that is interested … I did a quick sensitivity on this to see what my ROI would be if i increased my down payment.

Whats interesting (but not surprising) is my return on investment actually goes down as my deposit goes higher — contradictory to everyone’s opinion that you need to put 20% down. Not surprising because put simply, this is the power of leverage.

Conclusion

If you are not looking at your forever home and you are in a large metropolitan city, it often makes sense to rent and not to buy. What is important is that I have ignored price appreciation as the entire preface of this argument is that you use your money to buy real estate where the fundamentals make sense — not take your money and buy a brand new car.

Down Payment Sensitivity Table: