Tips and Tricks on Financing Real Estate

Along the way I’ve learned a lot about the financing demands in real estate investing. Below I have compiled a few of those lessons learned, struggles over the years and tips for you so you hopefully do not have the same ‘ah ha’ moments as me too late into the game. I am not a mortgage broker so make sure you reach out and actually discuss this with a professional.

To put it very simply, if I could not use 100% debt financing, I would not have a single property. I am far from any sort of trust fund baby and I do not make a killing in my day job. I published another article on how I bought my first property at 23 which outlines how I have used debt along the way.

Here is a more recent example. On April 30th, me and my business partner bought a duplex. For my share of the capital investment I financed the down payment through debt using my personal lines of credit. I knew the property was significantly under market value and with a few strategic renovations I would be able to recoup the full down payment + renovation costs. The bank provided a standard mortgage on 80% loan to value. I then pulled from another bank (through my unsecured line of credit) for 50% of the down payment on the property. My business partner did the same thing and pulled from his own line of credit for his 50%. Pretty awesome if I do say so myself 🙂

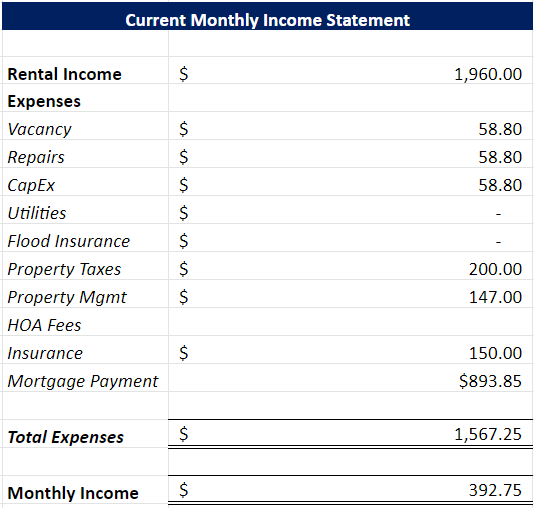

Duplex purchase price: $260K. Downpayment: $52K at 6% = $260 per month interest. Take a look at the table below below to understand how the property supports this strategy (cash flow > interest on my down payment). Eventual cash flow from turning around the units will be a lot higher (projected to be $1K+ per month so even if I never settle the down payment through a refinance I will be able to settle it just using the cash flow).

If you are using LOC’s make sure you have an exit strategy. How will you settle the debt? Will you sell the property or refinance it with the bank or something else?

HELOCs (home equity line of credits) are another great source of down payments if you already own real estate. Often we sit on equity that we have paid down through years of home ownership. This is essentially dead money since it earns you nothing and reduces your ROI. You do not want dead money. You want your money to earn you money. One way to ensure this is to tap into your HELOC’s and use this as a down payment for your next purchase. Scotiabank recently announced they would not use HELOC as a source of down payment, so you need to make sure these funds are sitting in your account (to be safe) for 90 days prior to purchasing your home.

When you are purchasing a home try to use a mortgage product that allows you to access the principal that you have paid down over the years as a line of credit. Scotiabank has this product it is called a STEP (ask your advisor about this). To my understanding BMO also has a similar product.